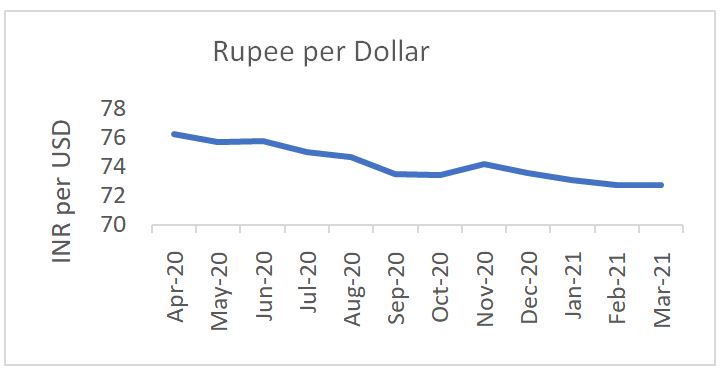

Rupee emerged as the worst performer among Asian currencies in April. As the dollar continued its rally, the rupee even fell to 75.31 against the dollar. Rupee has been appreciating against dollar, since last April. For instance, in April’20 due to the impact of Covid rupee breached 76 per dollar. Yet, rupee recovered from the fall and reached 72.79 per dollar in March’21.

However, the trend has reversed now. Various factors have played in tandem, pulling the rupee down against the dollar.

Second wave of the pandemic

The second wave of the pandemic has created an uncertainty in the near-term growth prospects of India.The economy was slowly recovering from the pandemic-induced economic crisis. However, the spread of the coronavirus has put a dent on India’s recovery path. As per the estimates of the RBI, the Indian economy is expected to register a GDP growth rate of 26.2 percent in Q1FY22. In the midst of the second wave, possibilities are high that the GDP growth rate for the first quarter would be revised downwards. Similarly, the contraction in Index of Industrial Production (IIP) at 3.58 percent in February’ 21 questions the pace of the economic recovery. The localised lockdowns to control the spread of the virus could further slowdown economic activities in the country. Similarly, inflation rate as measured by the Consumer Price Index (CPI) is also at a high level, though it is within the target range of 6 percent. Localised lockdowns could lead to supply-side disruptions leading to inflationary pressures in the economy. In such a scenario, pressure on the rupee would be high.

Rebound in the US economy

The US economy is emerging strongly from the crisis. The economic indicators are also supporting the fact that the US economy is strongly rebounding from the crisis. For instance, unemployment rate in March fell to 6 percent. Inflation rate also breached the target level of 2 percent, supported by both the fiscal and monetary stimulus. In this background, US-10-year bond yield is moving up. If yields are going up, one could expect a reverse flow of funds from the emerging markets to the US. Investors would be getting a decent return by investing in a risk-free asset like US bonds than in emerging markets. This partly explains why FPIs are turning net sellers in the Indian market. The uncertainty on India’s economic recovery as Covid cases are rising is also pushing the FPIs away from India.

Dovish monetary policy stance

In the last MPC meeting, RBI governor assured that the Central Bank would continue with the accommodative stance as long as necessary to push the economy back to the growth track. The Central Bank also announced one of the highest bond purchase programs, G-sec acquisition program (G-SAP). In the newly announced program, the Central Bank commits itself to the purchase of a specific amount of government securities. For Q1FY22, RBI would be purchasing INR 1 lakh crores worth of government securities. The loose monetary policy stance of the RBI also leads to the depreciation of the Indian currency.As the Covid cases are rising, RBI would continue with its loose monetary policy stance, putting pressure on the rupee.

Impact on the domestic economy

A falling rupee would be good news for the exporters but bad news for the importers. Theoretically, as the currency depreciates, exports would become cheaper. As exports become cheaper its demand would increase, giving a boost to the exports sector. This, in turn, could have a multiplier effect on the economy. In the current scenario, whether currency depreciation would be a boon for exporters largely depends on how well the global demand is picking up. However, it would make our imports expensive, especially crude oil imports. India is one of the largest importers of crude oil, and imports nearly 80 percent of its fuel needs. Increasing crude oil prices could lead to a general increase in the price level.

What’s ahead?

India’s forex reserves have reached an all-time high of USD 581.4 billion. It gives ample space for the RBI to intervene in the market, if the rupee falls to an uncomfortable level. However, the RBI would wait and watch before intervening in the market. As the inflation rate in the US is climbing up, there is uncertainty in the direction of the Fed’s monetary policy stance. In this background, Central Banks in emerging markets should be prepared to avoid another episode of the taper tantrum of 2013.