Liberalization initiated in 1991 marked the turning point for the Indian economy paving the way for sustained growth of the economy in the years that followed. The opening up of the economy required structural changes in many sectors. As part of these structural reforms in all major sectors of the Indian economy, the financial sector too witnessed initiation of liberalization. Within the financial sector reforms, capital market was a segment that was subjected to sweeping reforms. A major capital market reform was the opening up of the mutual fund industry to the private sector. Earlier the industry was dominated by UTI, which was the monopolist in the industry for long, and the PSU insurance companies and some PSU banks.

Liberalization initiated in 1991 marked the turning point for the Indian economy paving the way for sustained growth of the economy in the years that followed. The opening up of the economy required structural changes in many sectors. As part of these structural reforms in all major sectors of the Indian economy, the financial sector too witnessed initiation of liberalization. Within the financial sector reforms, capital market was a segment that was subjected to sweeping reforms. A major capital market reform was the opening up of the mutual fund industry to the private sector. Earlier the industry was dominated by UTI, which was the monopolist in the industry for long, and the PSU insurance companies and some PSU banks.

Private sector was allowed entry into the mutual fund industry in July 1993 and the first fund was launched by Kothari Pioneer, a joint venture between Chennai based Kothari group and the US based Pioneer. Kothari-Pioneer was later sold to Franklin Templeton. Kothari-Pioneer deserves credit for introducing Daily NAVs and Monthly Portfolio Disclosures, which were path-breaking initiatives at that time. Kothari-Pioneer was followed by Morgan Stanley, JM and the Birlas.

Some of the early schemes have done well. The two schemes started by Kothari Pioneer in December 1993 (now Franklin Templeton Blue chip and Franklin Templeton Prima) have a fabulous track record of delivering 20.90 and 20.30 percent CAGR since inception. Morgan Stanley mutual fund which aroused huge market expectations disappointed with meager returns of 8.9 percent CAGR since inception. It is important to note that the oldest equity mutual fund scheme, UTI Master Share, has grown at 18 percent CAGR since its launch in 1986. This is good performance compared to the 14 percent CAGR for Sensex and 6 percent CAGR for gold during this period.

25 years after the opening up, the industry has come a long way. Now the top players are the private sector majors like ICICI Pru, HDFC, Birla Sun Life and Reliance followed by SBI and UTI. The AUM of the industry has grown to Rs 23 trillion, which is around 20 percent of the bank deposits in India.

Though the growth of the industry has been impressive, it came in for severe criticism for proliferation of schemes through NFOs, which were easy to market, and mis-selling by distributors.

The growth of the industry during the last 5 years has been very impressive. Poor returns from bank FDs and lackluster real estate market favored the growth of the industry. Campaigns like ‘Mutual Funds Sahi Hi’ and financial literacy initiatives from mutual funds and stockbroking companies came as a shot in the arm for the industry.

A big takeaway from mutual fund performance is that SIP is the ideal strategy for retail investors. SIPs have given excellent returns in the long run. Study of equity diversified funds with a history of more than 10 years has shown that there is 94 percent chance of positive returns in 4 year SIPs, 90 percent chance of positive returns in 3 year SIPs and 84 percent chance of positive returns even in 2 year SIPs. As the time horizon extends, the probability of high returns increases substantially.

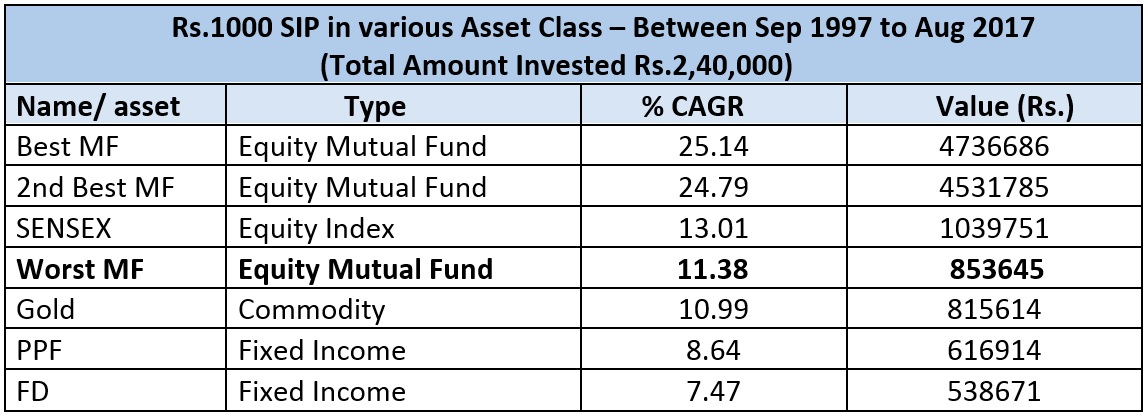

SIPs in equity funds have out-performed other asset classes by a wide margin. Data showing SIP returns during the last 20years from various asset classes is revealing.

During this 20-year period systematic investment every month delivered 13 percent for Sensex, 11.38 percent for the worst performing fund and a fabulous 25.16 percent for the best performing fund. 15 equity mutual funds returned more than 20 percent CAGR. Compared to returns from fixed income and gold, this is excellent outperformance.

The best is yet to be

For the Indian mutual fund industry, the best is yet to come. Even though the industry has grown impressively in recent times, the potential is huge. Mutual fund penetration in India is even now very low with AUM at 10 percent of GDP compared to the global average of 55 percent. The share of mutual funds in financial savings also is very low at 2.9 percent compared to 40 percent in currency and deposits. The AUM of the industry grew by 18 percent a year during the last decade and is projected to grow at 20 percent a year during the next 5 years. Going by the present trends the AUM of the industry can grow to around Rs 66 trillion by 2023, almost tripling from the present levels. As the Indian GDP grows from $2.5 trillion presently to around $ 5 trillion by 2025-26, corporate profits also are set to grow impressively. The historical average of corporate profits to GDP has been around 5 percent. This can translate into corporate profits of $ 250 billion or Rs 17 lakh crores by 2025-26. Simply put, some 12 lakh crores of corporate profits are likely to be generated in India in the next around 8 years. This is an unprecedented historical opportunity for investors in India. The simple way to participate in this potential wealth generation is to invest in mutual funds, preferably through SIPs.

{kind=link}

Good Article.

Short-term market fluctuations are common. Hence, it is important to maintain a long-term investment horizon in equity investments. Over a period, the market cycle is expected to change and soon the fund would rally upwards with the market. We have seen this happen in the past, hence, is expected to happen in future as well. It may take a few months or even a few years. All that is required is patience. Thanks for sharing a great artcile