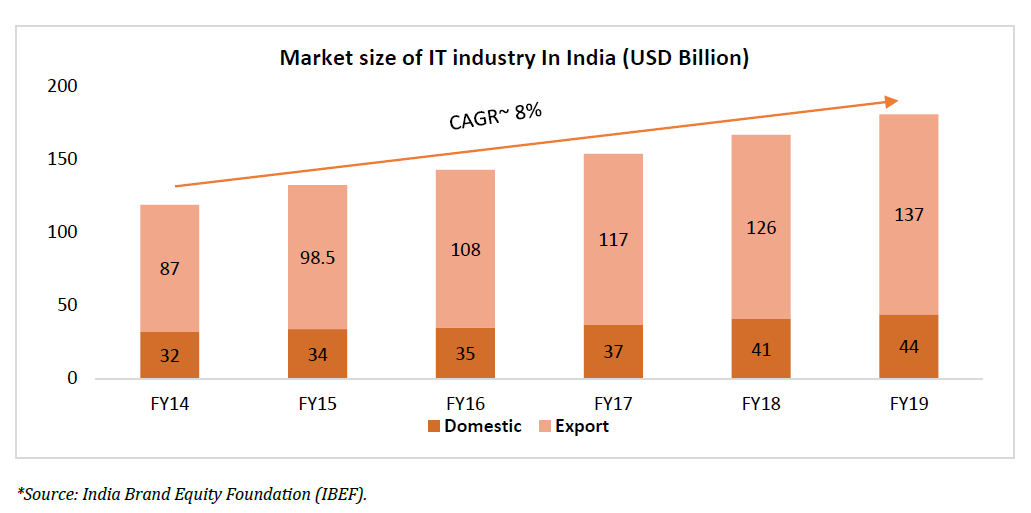

With a big breakthrough in the 90’s, Indian IT industry has been going through a paradigm shift. From a provider of punched cards to writing codes (KPO), developing software and application for multinational companies, the sector has grown to a full package service provider like ER&D (Engineering Research and Development). India enjoys close to 55% market share of the US $185-190 billion global outsourcing business in 2018-19, as per publication by India Brand Equity Foundation (IBEF). Both the software and hardware sector in India attracted cumulative Foreign Direct Investment (FDI) inflows worth US $37.23 billion between April 2000 and March 2019 as per the data released by Department for Promotion of Industry and Internal trade.

Hit by macro concerns

However, IT industry in India has slowed in the last five years to a revenue growth of 8% CAGR. After many years of good performances, a lot of negative factors related to macro and micro level impacted the sector. Strict H1B visa norms in US, drastic decline in visa approvals impacting acquisition of new businesses, increasing cost and weak discretionary spending squeezing growth of order book impacted the industry. The main stream IT companies found support from marque clients but mid-cap companies were hurt by slowdown in global economy. Other macro negatives were adverse cross currency changes, in which USD strengthened against key currencies like GBP, EUR and AUD. Brexit fears impacted discretionary spending in UK while economies also slowed in Europe, US and Emerging Markets.

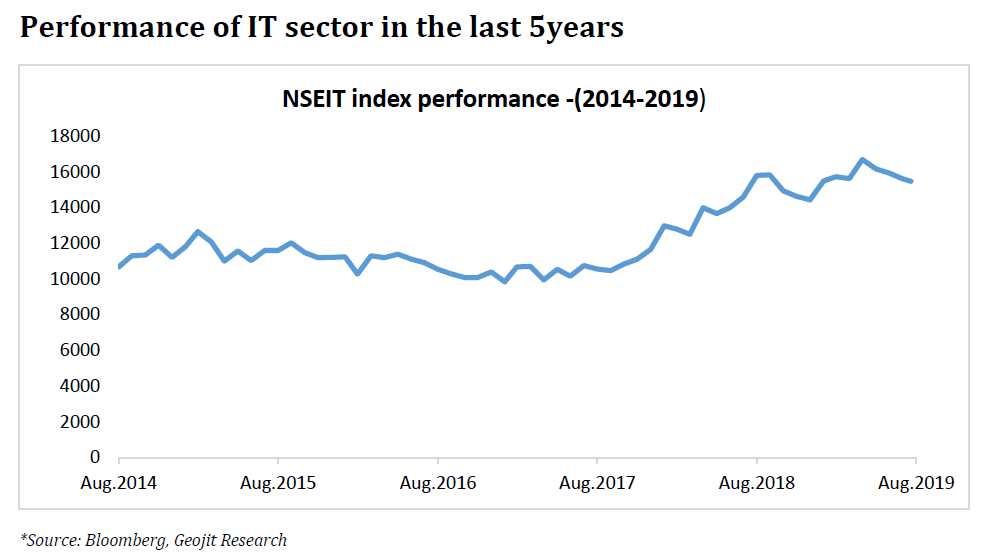

Weakness in rupee due to strong dollar and macro related tension had a positive impact on the sector from 2013 to early 2015. However, the same didn’t continue from 2015 to 2017 as measures by RBI arrested fall of rupee and weak global IT spending hurt performance. Companies opted for job cuts during that phase in order to support margins. From 2017 the scenarios got changed as companies started changing the focus to digital and growth improved in the US market. Global IT sector growth increased from 3.8% in 2017 to 5.2% in the early 2019 as per Computing Technology Industry Association (CompTIA) research. National Association of Software and Services Companies (NASSCOM) has lowered IT service export growth from 12-14% during FY16 to 9% in 2019 due to uncertainties in the sector.

Considerable revenue growth for Tier 1 in-spite of margin concerns compared to Tier 2 players

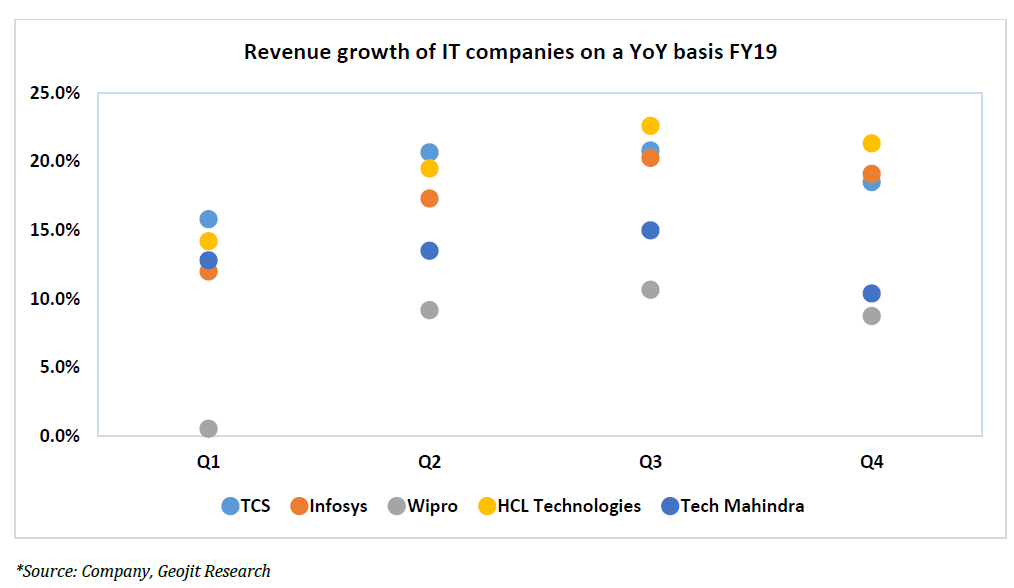

Revenue growth of the Tier 1 companies like TCS, Infosys, Wipro and HCL Technologies has been on the higher side, in the range of 8-10% in dollar terms. This was largely fuelled by proper client mining and order wins in their respective segments. While for Tier 2 companies, excluding Mindtree all other companies reported a low single digit revenue growth. Banking and Financial Services Industry (BFSI) which contributes closely 30-35% of revenue mix reported single digit growth for major players in the range of 8-9% for FY19.

There was a time when IT companies laid off workers due to slowdown in growth but now the scenario seems to be different. With restriction being placed over H1B visa allotments many IT companies have been compelled to hire local talents from U.S, thereby increasing their wage cost and impacting margins. There has been a 100-150 basis point volatility in margin of IT companies due to these factors. Largely client specific concerns can also be attributed to the margin drop. TCS and Infosys were able to post decent set of margins led by operational efficiencies. Sharp fall in sub-contracting cost improved margins of selected IT players like Wipro. While for HCL technologies further acquisitions diluted margins. Margin concerns for tier 2 players was higher compared to tier 1 due to cost pressures.

Recent quarter performance and the new trend

No difference was found in the Q1FY20 results other than some companies trying to increase the revenue growth from the traditional businesses to digital. Earnings growth was visible on select players while other companies remained on the backseat.

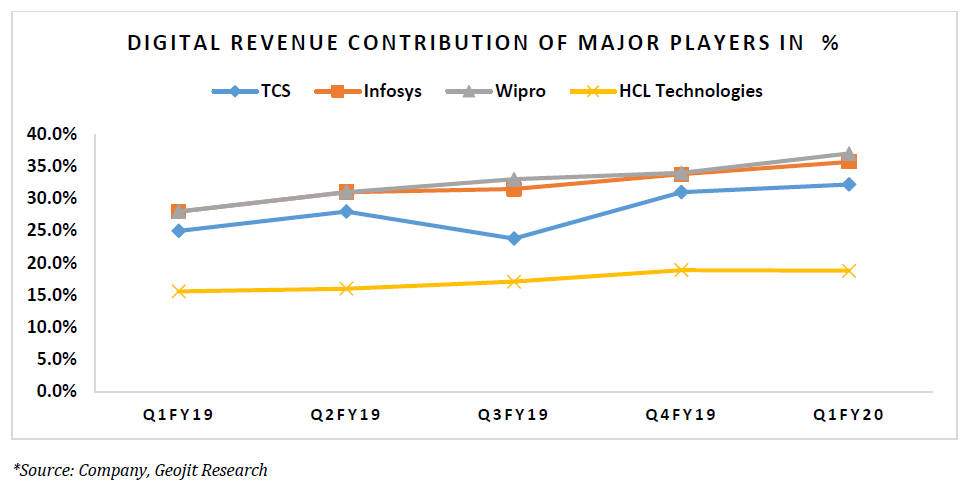

Digital service is the new trend of the IT sector. Digital business involves offering services and products by harnessing new technologies such as Automation (Examples: Using digital devices to track patient monitoring in hospitals, using system to track the fuel dispenser where the owner can easily track the status of the stock lying in the inventory and trigger refuelling after certain levels). IOT –Internet of Things (Controlling the ceiling fans and lights in home/office on convenience using connected devices like mobile phones or other hand-held devices like voice command gadgets). Artificial Intelligence (Using algorithms and process to refine data in a particular website to improve customer experience Example: AI powered matrimony websites), big data and cloud computing to block chain. Significant part of the major IT Companies’ innovation effort will be focused on building expertise in the digital services.

There has been a shift among the clients to focus on digital platforms that has forced companies to change their business model. Even though a big jump is not witnessed on the revenue front, a change in revenue mix from traditional to digital is the key for major players going ahead. Companies like Wipro which has higher exposure to digital found it difficult in converting that into their revenue due to client losses.

Cost concerns to hurt

Despite all the weaknesses surrounding the sector, valuation doesn’t look so attractive with one year forward P/E at 20x. Factors like buybacks and defensive tag urged investors to hold on to the stocks. Concerns due to weakness in dollar over fears of recession in the U.S, slowdown in global economy and higher visa cost will impact revenue and margins ahead. With government bringing strict norms by increasing taxes for buybacks, we expect the companies to refrain from buying back shares from the public. On the earnings front we expect Infosys, TCS and HCL technologies who have been increasing presence in the digital space with big billion-dollar clients to stand out in the industry.