by Vinod Nair

During the first half of November we were seeing a disagreement in the trend of the market. The Market has been very positive till the end of October; but as the conclusion of Q2 results depicted an improvement in earnings growth, market has been deceptive. Over the last 3 years market valuations have been expanding, expecting an improvement in economic and earnings growth, which did not happen for a very long-time. The earnings growth of main indexes has been very flattish. During FY15 to FY18 the annualised growth has been only 5% while market has been up by 50%. From the recent all time high, Nifty50 has declined by 3%, Nifty100 by 4% and Nifty Small-cap by 5% (as on 17th Nov). The strength of this fall is not completely explained by the main indexes since many high quality and growth-oriented stocks are down in a range of 10% to 20%. Some good performers amidst this fall were IT, Private banks, Auto, FMCG, Chemicals and Consumer Durables due to supportive factors like INR depreciation, defensive nature of investing in staple industry and remedy from NPA and GST issues.

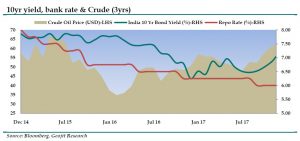

Two main factors which impacted the performance of the domestic market were increase in 10 yr yield and crude prices. The 10 years benchmark Government security yield has increased to 7.05% which is 70bps up from the low since June 2017. The trend has become more volatile since the more hawkish view by RBIs during Aug-Oct policy. The prospects for a rate cut in the near future is diminishing.

10 year yield, bank rate & Crude (3yrs)

Main factors that are leading to hike in yield are inflationand expectation of increase in US FED rate. CPI has been continuously increasing over the last 6months. October CPI stands at 3.58% while core inflation is up to 4.6%, which is at the upper end of the 4.2% – 4.6% range forecasted by RBI. Crude oil prices are at 2year high and have doubled from the low in the last 1year to a high of US 64/bbl. This trend will develop as per the progress in the Middle East which is very difficult to extrapolate now. But we can assume that production from US shale will increase and retail petrol and diesel prices in India will be adjusted by a reasonable cut (not completely) in excise by the government as cost of crude increases for OMCs. The new Fed Chair designate Jerome Powell will replace Janet Yellen by January 2019. The rate is likely to be increased in December 2017 and 2 to 3 times more during CY2018. As a result INR has started to depreciate in culmination of fear from the increase in fiscal deficit and higher supply of government bonds due to oil prices, higher govt spending and cut in GST rate.

The concerns over fiscal deficit appear to be overblown since the benefits from reforms will flow over the next 1-3years. Rating upgrade is a strong response to the critics. International rating agencies were waiting to see the implementation of new reforms, re-capitalisation of PSUBs and restructuring of NPAs in the Indian banking sector. As the implementation of transformative decisions are progressing and government’s spending and deficit plans are encouraging, Moody’s decided to upgrade the India rating, which was overdue. We understand that FIIs were net sellers till the announcement of re-cap and bharatmala by the government of India. FIIs have turned net buyers with inflow of~ Rs22, 500cr since 25th October to 17th November. We feel that this trend is likely to continue, bond yield will decline and India will outperform in the long-term.

A consolidation will be good for the market… in the long-term

Well, for the retail investors it is a good time to chip into the market slowly and consider adding good quality stocks, which are available about 10% to 15% lower than they were a month back. This consolidation may continue for some more time while the overall expectation from market return is moderated compared to the equity euphoria seen over the last 3years. Three reasons for a moderate return in equity are reduction in global liquidity, increase in global bond yields and premium valuations. At the same time, since global and domestic economy are likely to improve and domestic liquidity is maintained solid, this will provide enough legroom for good stocks to perform well. We can expect well managed entities (shift in business from unorganised to organised), growth sectors due to change in domestic and global demand (Defence, Chemical, Textile, Metals, Housing, Exports) and value buying (Pharma, IT, Telecom) will maintain the attractiveness of the equity market.

The review of Q2FY18 is good… stating improvement in H2FY18

Q2 expectation for PAT growth was 6%, 14% and 13% for Sensex, Nifty50 and BSE100 respectively. If we adjust one time losses and expenses, the actual growth is about 5%, 10% and 14% respectively. We should consider these numbers as good, because about 45% of the results are above expectations and bad results are for those companies which had poor expectations. Given the positive commentary and improvement in the actual economy, market may marginally increase the forecast for H2FY18 and FY19. For Q2 the good performing sectors were Finance, Chemicals, Cement and Metals. Neutral performers were Auto, FMCG and Oil & Gas; the poor performers were Power, Telecom, Pharma and IT.

The market seems to have largely factored-in the intermediate dip in earnings and discounted the scenario forFY18. It is looking to and beyond FY19, given the increased spending plan, ease from GST disruption, benefits to organized sector and supportive global trend. Every dip is being used as an opportunity to buy while valuation is following the price given better prospects for domestic macros.

{kind=link}