by Mahesh Vyas

by Mahesh Vyas

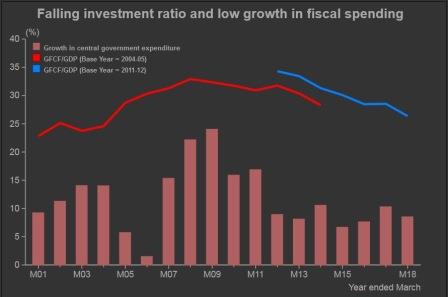

Central government expenditure is expected to grow by 12.3 per cent in 2017-18 and then by 10 per cent in 2018-19. These growth rates are not good enough to help the economy bounce back to a higher growth trajectory. More pertinently, it is unlikely to help arrest the consistent fall in the investment ratio.

The investment ratio has been falling for a decade now. It does not look like its fall will be reversed or even arrested by itself for a long time. Therefore, a fiscal push is perhaps, worth considering. Budget 2018 does not provide any support to raising or arresting the fall in the investment ratio.

Demand, as seen in the capacity utilisation of the manufacturing sector and the plant load factor of thermal power plants, is very low – at about 70 per cent and 66 per cent, respectively. Till these rise by 10 to 15 percentage points each, there will not be a compelling economic reason for new investments to come in. Without a pickup in investments, growth is unlikely to accelerate or even maintain its current rate. It is therefore imperative that growth is re-ignited using a fiscal push.

The investment ratio has fallen sharply from 34.3 per cent in 2011-12 to 26.36 per cent in 2017-18. During this period, actual central government spending has grown in single digits per annum. In contrast, central government spending had grown at a much faster pace in the earlier years. And, during these years, the investment ratio did not slide as sharply.

Central government expenses had grown at the rate of nearly 20 per cent per annum during the period 2007-08 to 2011-12. This helped stave off the challenges faced by the Indian economy following the global financial crisis in 2008. Increased government spending worked counter-cyclically to the declining investment ratio. Nevertheless because of the sustained increase in the investment ratio over a decade or so, it declined from 32.9 per cent in 2007-08 to 31.8 per cent in 2011-12 (old series) implying a drop of 0.29 percentage points in the investments ratio per year. Without the fiscal push, this decline could have been much steeper.

This is evident in the subsequent period when without fiscal support the investment cycle fell sharply. During the period 2011-12 through 2017-18 the investment ratio fell much more sharply – from 34.3 per cent to 28.5 per cent (new series) implying a drop of 1.2 percentage points in the investments ratio per year. Effectively, the rate of fall in the investment ratio since 2011-12 is four times the rate of fall in the same during the four years till 2011-2.

Average growth in government spending was only 8.7 per cent per annum during the period 2011-12 through 2017-18 compared to the 20 per cent per annum earlier. The sharper fall in the investment ratio during recent times when the investment ratio has been falling warrants a larger fiscal push to offset its debilitating effects on growth and employment.

Modi Sarkar has been conservative in increasing central government spending.

The average increase in government spending during the tenure of the Modi Sarkar has been of the order of 8-9 per cent per annum. This is significantly lower than the 13 per cent per annum growth that UPA governments (I and II) and what the Vajpayee governments achieved.

Increased government spending does not necessarily mean a higher deficit or even higher taxation. It is important to raise non-tax and non-debt generating resources to fund a higher government spending regime. This can be achieved through aggressive disinvestment and higher non-tax revenue receipts.

Central government expenditure is budgeted to increase by 10 per cent, which is nearly Rs.3 trillion in absolute terms. We would need an additional Rs.1.3 trillion to raise the growth in central government spending by 20 per cent. This is the rate at which a fiscal impetus starts to take effect. Disinvestments brought in Rs.1 trillion, largely through a sleight on the hand. It should be possible to raise the additional resource through an honest and aggressive disinvestment program to provide a fiscal push without raising the fiscal deficit.

Modi Sarkar is conservative when it comes to disinvestment. It seems to be clearly shy of privatisation and therefore of aggressive disinvestment. A strong government with a mandate to drive economic growth and a commitment to minimum government should have shown a greater willingness to get government out of the business of business and yet, drive business out of its current ebb.

{kind=link}